Which Central Bank will dare to increase interest rates 1% above inflation to fight inflation? Whilst I stand to be corrected, the International Monetary Fund demands this of those countries that it bails out.

Now consider the consumer that met the lender’s minimum requirements to qualify for a loan after March 2020 (when the RBA gifted billions of free money at just 0.10% to the banks) under the let credit flow freely mojo.

For this consumer, the interest rate buffer to service the loan may have been wiped out by the recent RBA rate increases, and the assessed household expenditure at the time may also have been wiped out by the cost-of-living inflation rise (fade the inflation figures the government statisticians publish).

If this consumer is close to or actually is in mortgage stress today, then consider all those consumers that are in the same predicament because they have bought into the housing upswing (fuelled by cheap money and promises by the Reserve Bank). They got even bigger mortgages on similar lender interest rate buffers and expenditure, and worse, they may have borrowed up to 95% of the home purchase price.

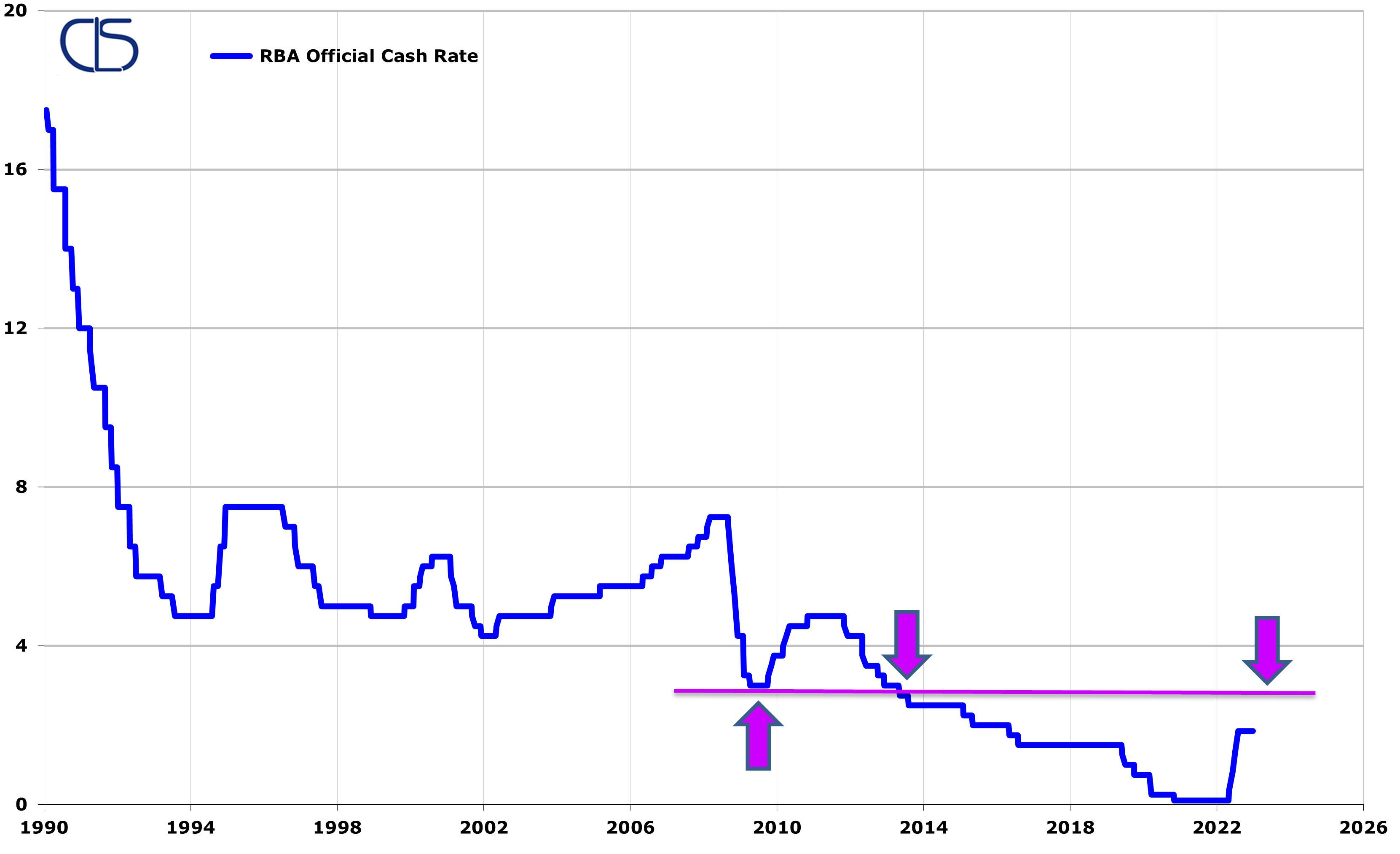

Our 4 June 2022 view remains the same, and we now have an avid supporter, the 3 month Bank Bill Swap Rate (BBSW), currently at 2.45% on an RBA official cash rate of 1.85%, which implies a 0.50% increase in the cash rate on Tuesday, 6 September 2022.

The 3mth BBSW rate hit a low of 3% (support in technical analysis language) in the heydays after the GFC, then rebounded to circa 5.50% (resistance) and then smashed through support at 3% (now acting as resistance) to the historical low of just 0.09% during the height of the Covid years. See below chart where the magenta hand drawn line is.

Technical Analysis says that the 3mth BBSW rate will find it hard to get through the 3% resistance level on its first attempt unless the up and coming implosion of the bond market occurs now, and 10-year government bond yield explodes higher and severely breaches the levels we have outlined in our 4 June 2022 note.

Ditto, for the RBA cash rate, currently at 1.85% (below chart).

Another critical supporting factor is the US stock market may be required to be significantly higher heading into the mid-term US elections in November 2022.

This would need a certain tool to manufacture a rise, and the only way this may be achieved is for the Federal Reserve to bring to a halt interest rate rises after the next increase (likely September 2022), and thereafter lowering the US Treasury 10-year bond yields using its tool.

Our view is that the Reserve Bank will pause its interest rate increases after the next increase, for at least until the first quarter of 2023, and reassess afterwards. Until proven wrong or the market indicators we use change or both, this view is maintained.