CONCLUSION TO THIS RESEARCH NOTE

» We are of the opinion that staying variable far outweighs fixing for a term of 2, 3 or 5 years.

» The 24 March 2022 view remains unchanged – RBA to increase rates by about 1.75% to 2.00% and then pause for 6-12 months to see how the consumer and the economy survive being hit with cost of living inflation and interest rate rises.

» The RBA last increased rates by 0.25% on 3 May 2022 but is far behind other central banks, and with inflation at 5.1% the RBA may increase rates by 0.65% or more at its next meeting on 7 June 2022.

» Our reasons on what we base our views on are below, and when the dust settles, should we be correct, it will represent a better opportunity to fix your home loan interest rate, because from there the probability of the USA bond market imploding is real and it will take other bond markets along with it.

THE DENIAL

On 14 September 2021, the Reserve Bank (RBA) Governor, Philip Lowe, was adamant that interest rates will not rise until at least 2024. Yet on 2 May 2022, seven months later, the RBA was forced to increase interest rates by 0.25% (more increases pending) to fight inflation and amidst a federal election.

At the time we beg to differ, and we were correct.

TODAY’S HYPE

The Johnnies come lately are now boasting that the RBA will keep on raising short term interest rates, and that long term interest rates will keep on rising.

IGNORE THE HYPE

For any central bank to fight inflation it must have the courage to do what former FED Chair Paul Volcker did in the late 1970s and early 1980s – raise interest rates well above inflation. And it’s not going to happen soon, because it will kill the economy and demolish the consumer.

TODAY’S VIEW ON LONG TERM INTEREST RATES DIRECTION

We first alerted the need to consider fixing your home loan interest rate on 15 December 2020, followed on 28 February 2021, and again on 18 October 2021.

It was such a success that we had a lot of clients that considered our advice at the time and fixed their loans and together with other clients that did not, asked us what we based our views on.

Information you will not get elsewhere In this update we decided to share what we base our views on and our reasons why we expect long term interest rates to be close to a temporary peak and why they are about to make a move lower, which will impact on how much the RBA (and the FED) will increase short term interest rates. The information we rely on and provide below are for educational purposes only and is not advice.

It is technical in nature, and you may not fully understand the indicators we use, but we have good indicators.

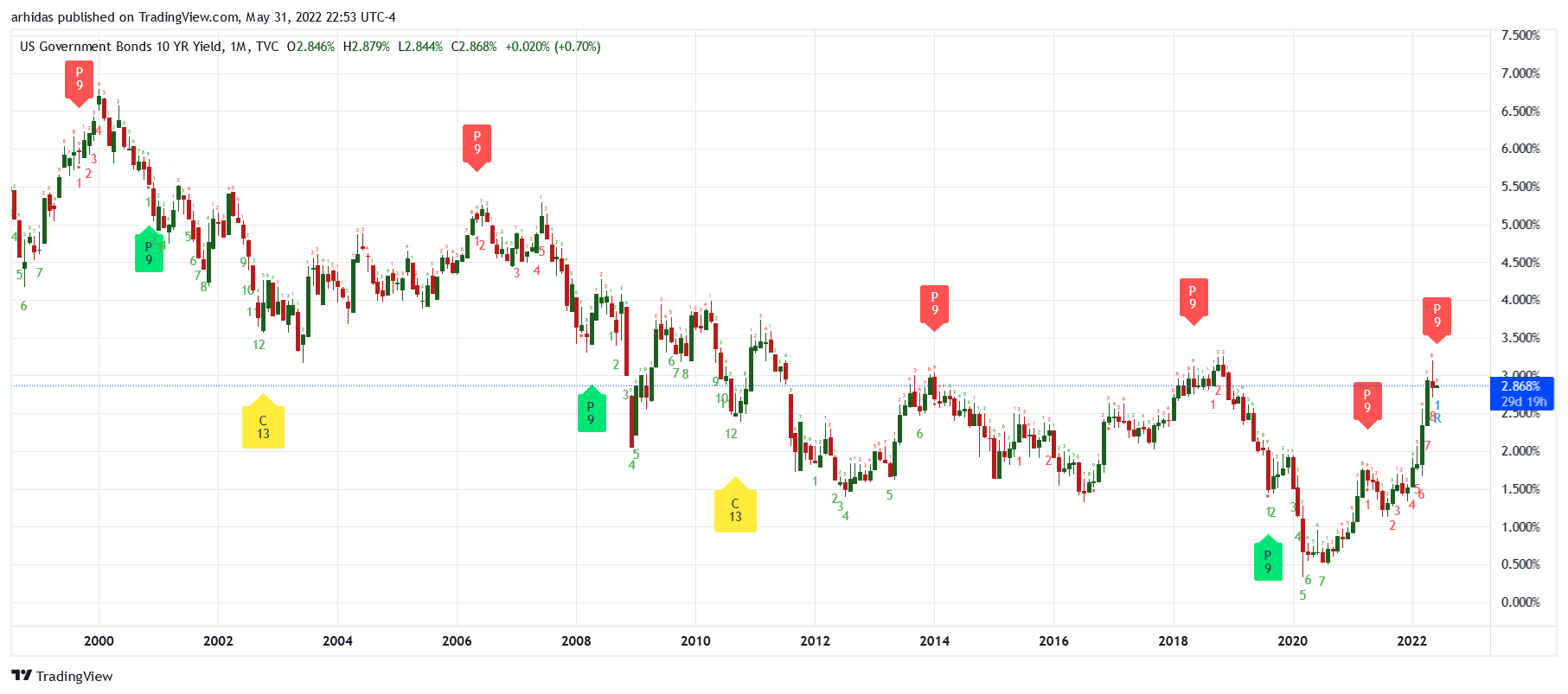

USA Government 10-year bond

The below chart is the monthly (each bar is one month’s worth of trading data) USA Government 10-year Treasury Note yield.

Australian Government 10-year bond

Note how closely the correlation between the Australian Commonwealth Government 10-year bond yield is with its US equivalent.

One of the indicators we are basing our views on

Now let’s overlay both charts with technical analysis indicators. This indicator alerts ‘price exhaustion’ and often occurs at or near reversal points on charts and is shown with a red P9 in the below charts. The first chart is the USA 10-year bond followed by the Australian equivalent.

Every time a red P9 indicator formed on the USA 10-year bond monthly chart, there was a substantial or notable fall in interest rates, viz, 1999, 2007, and recently in 2014, 2018 and 2021. Sure, the market can move sideways for a while, but why would it be any different today?

CAVEAT The red P9 indicator formed for the month of June 2022 and the conditions which it formed under must hold true till the end of the month, otherwise the P9 indicator will vanish, which will invalidate our research. The probability of it completing the formation is relatively high.

The reverse usually happens when a green P9 indicator forms, which together we other indicators we use, we alerted the need to consider fixing your home loan interest rate on 15 December 2020, followed on 28 February 2021, and again on 18 October 2021.

The USA Dollar Index – the DXY

Supporting our view is that the market fear trade (seen in the last year) into the safety of the US Dollar (as the world’s reserve currency) is waning. A red P9 indicator has formed on the monthly chart in April 2022, on the weekly chart ending 29 April 2022, and on the daily chart on 28 April 2022. When all major time frames form ‘price exhaustion’ signals, we take note.

A fall (and not a crash – the crash will come later) in the US Dollar may trigger a shift out of cash into bonds and stocks and more ‘riskier assets’ (again this is not advice), which is another reason we believe that long term interest rates can move lower from current levels and present a better opportunity to consider fixing your home loan.

THE BRUTAL REALITY ON LONG TERM & SHORT-TERM INTEREST RATES

When the USA bond market implodes, and it will (again this this not advice), long term interest rates will uncontrollably explode higher and will be followed by short term intetest rates. I cannot say what will cause this but it may start when the USA 10 year bond yield explodes through the 3.25% level (red horizontal line) on the below chart.

The Federal Reserve has unequivacally earmarked two consecutive 0.50% intetrest rates hikes, which will take the funds rate to 2% whilst inflation is 8.5%.

The next FED meering is on 15 June 2022 and the probability of the FED pausing rate hikes circa September 2022 is increasing, and if they do, expect ‘risk assets’, especially the stock market, to explode higher for one last hurrah.

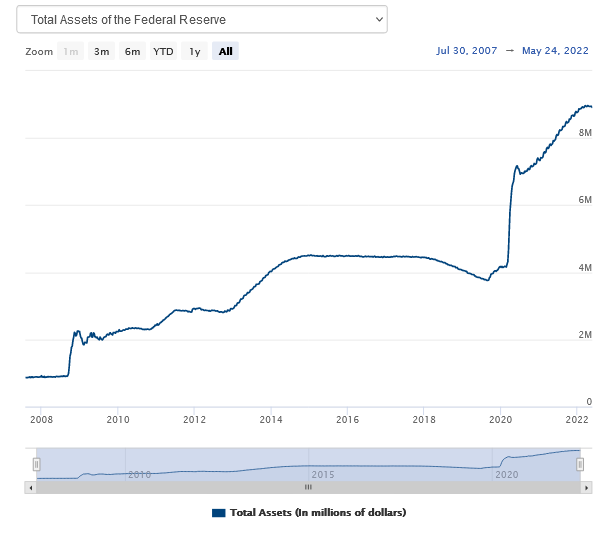

Also, the FED has commenced Quantitiative Tighetening (QT2) on 1 June 2022 to shrink its USD$9 trillion balance sheet.

What it means in practice is that there will be a brief period of balance sheet shrinkage before the ‘next big crisis’ emerges and the FED blows up the balance sheet again.

Together with the US budget and trade deficits will perhaps be the cause of the bond market implossion.

It’s all about fixing at the right time Months before the bond market implodes or interest rates rise again after they fall, and you are fortunate enough to have fixed your home loan, either by luck or by good advice and information to make informed decisions, you will be far better off than others.

Other than the red P9 indicator we summarise above, we also need to see a SELL signal (for lower interest rates) on the daily, weekly, or monthly charts or all of them.

Currently, the Australian 10-year bond has a BUY signal (signalling that interest rates can go higher) on the weekly chart (below) – it’s been going sideways for the last 5 weeks, and this week higher because of the RBA meeting next week – and need to take out the green dots of support (within the drawn circle on the chart) to get a SELL signal (for the commencement of lower interest rates).

When we get a SELL signal, interest rates will move lower, and this will represent a better opportunity to consider fixing your home loan when we next get a BUY signal, and we will alert you of this - but you need to be either a client or follows us on social media or return back here!

Thank you If you liked this research note, it’s information that you will unlikely get elsewhere when you ask whether it is time to fix your home loan, please share with friends and relatives, and please refer them to us for their home purchase and loan. And we also offer complimentary property research, auction bidding and negotiations with real estate agents.

We do not pay kickbacks for referrals to real estate agents, accountants, solicitors, financial planners, or anyone else, and we rely on our clients for referrals.

If you have any questions, please let us know.

TODAY’S HOME LOAN INTEREST RATES

Market competitive (lender dependant) owner-occupied home loan interest rates today would be about –

variable 2.45% compared to 2.45% in May 2021;

2-year fixed 3.80% today compared to 1.85% in May 2021;

3-year fixed 4.44% today compared to 1.90% in May 2021; and

5-year fixed 4.99% today compared to 2.00% in February 2021.