THE UNKINDNESS CUT POST RBA

On 3 November 2020, the Reserve Bank announced a reduction in the cash rate, 3-year yield target, and the interest rate on new drawings under the Term Funding Facility to 0.10% from 0.25%.

It also announced the purchase of $100b bonds and that it was not** expecting to increase the cash rate for at least 3 years.

Most lenders responded by slightly reducing their competitive and market aligned fixed interest rates whilst not passing a single 0.01% on their variable rate loans.

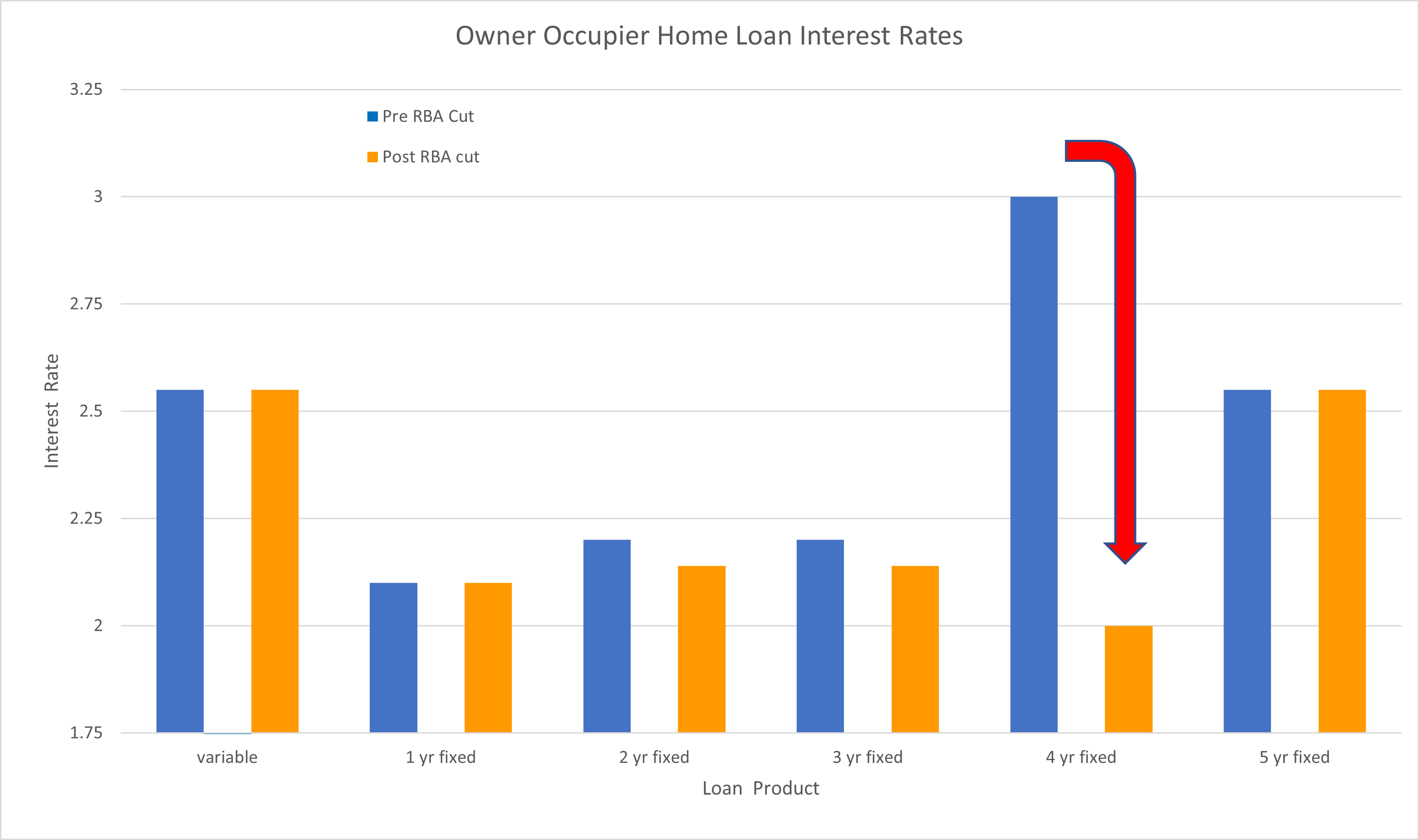

The unkindness cut of all was the reduction of the uncompetitive and way out of market 4-year term fixed interest rate, and it made media headlines for the wrong reason!

The graph shows the approximate change in interest rates, pre and post RBA.

When the dust settles, expect lenders to start offering lower variable interest rates for the acquisition of new customers.

I say this because the Reserve Bank stated ** and why would there be a need to rush to fix your home loan today unless the bond market signals otherwise.

You should consider fixing your interest rate to pick up yield (if it makes sense) or about 6 months before the Reserve Bank begins to increase the official cash rate.